How I Turned Moving Expenses into a Smarter Financial Move

Moving isn’t just about boxes and trucks—it’s a financial crossroads. I used to dread relocation costs until I realized they could be part of a smarter money strategy. What if your next move wasn’t just an expense, but a trigger for better financial decisions? This is how I shifted my mindset, controlled costs, and even found hidden opportunities in something I once saw as pure loss. By reframing moving not as a drain but as a pivotal moment, I uncovered ways to reduce waste, make value-driven choices, and align my spending with long-term goals. This journey wasn’t about cutting corners—it was about building clarity.

The Hidden Cost of Moving: More Than Just Boxes and Gas

Moving is often seen as a single, unavoidable expense—truck rental, a few boxes, maybe some help loading. But the true cost extends far beyond these visible items. In reality, relocation triggers a chain of financial obligations that can quietly erode savings if not anticipated. The average household underestimates moving expenses by nearly 40%, according to consumer spending reports, because they fail to account for indirect or delayed costs. These include security deposits on new rentals, utility setup fees, internet installation charges, temporary lodging if the move-in date is delayed, and even higher grocery bills during the first weeks in a new location when routines are disrupted. These seemingly small amounts add up quickly, turning what looked like a $2,000 move into a $4,000 burden.

One of the most overlooked expenses is storage. Many people assume they’ll pack and move everything in one go, only to discover that their new home isn’t ready or their old one sold faster than expected. Last-minute storage rentals can cost $100 to $300 per month, and without insurance, damaged or lost items aren’t covered. Another hidden cost is insurance gaps—renter’s insurance doesn’t always transfer seamlessly between locations, and some policies lapse during the transition. This leaves personal belongings vulnerable during the most physically chaotic time. Additionally, people often overlook the cost of replacing items they thought they had but lost in the shuffle: kitchen tools, cleaning supplies, even shower curtains and towels, which can easily add another $200 to $300 to the total.

The ripple effect also touches income. Taking time off work to pack, move, or handle logistics reduces paycheck earnings, especially for hourly workers. Even salaried employees may lose productivity during the weeks leading up to and following a move, affecting performance bonuses or career momentum. Furthermore, moving often disrupts side income streams—freelancers lose clients during transition, pet sitters or home-based tutors face cancellations. These indirect losses are rarely factored into the budget but can have a real impact on financial stability. Recognizing this full scope is essential. When you see moving as more than a one-time transaction, you begin to plan differently—anticipating, tracking, and managing each layer of cost before it appears.

Understanding the true financial footprint of relocation allows for better decision-making. For example, knowing that utility setup fees are common, you can call providers in advance to negotiate waived installation costs or bundle services. Awareness of potential storage needs encourages earlier planning—selling, donating, or downsizing before packing begins. Most importantly, seeing moving as a financial event, not just a logistical one, shifts your mindset from reactive spending to proactive control. This awareness is the foundation of turning a necessary expense into a strategic opportunity.

Why Moving Is a Financial Reset Button (And How to Use It)

A move forces change—and change, when managed well, can be a powerful financial reset. Unlike gradual adjustments to spending or saving, relocation disrupts the entire financial ecosystem. Routines break. Contracts end. Habits dissolve. This temporary instability creates a rare opening to rebuild with intention. Most people focus only on the logistics of the move, but the real value lies in the decisions made during and immediately after the transition. This is the moment to reevaluate not just where you live, but how you spend, save, and earn. A financial reset isn’t about starting over—it’s about upgrading your system based on current priorities and goals.

Consider housing costs. A new rental agreement is more than a monthly payment—it’s a chance to align your largest expense with your income and lifestyle. Moving to a lower-cost city might allow you to redirect hundreds of dollars each month toward debt repayment or retirement savings. Conversely, relocating to a higher-cost area could prompt the creation of a side income stream, such as remote freelancing or part-time consulting, to maintain financial balance. The key is to approach the move not as a passive event but as an active financial decision point. Even small changes—like choosing a home with lower utility costs or closer to public transit—can compound into significant savings over time.

Subscriptions and recurring expenses are another area ripe for review. During a move, many services naturally pause—gym memberships, streaming platforms, home delivery boxes. Instead of automatically renewing them, this is the ideal time to assess their value. How many were used regularly? Which ones fit the new lifestyle? Canceling unused subscriptions can free up $50 to $100 per month—money that can be redirected toward building an emergency fund or paying down credit card balances. Similarly, banking and financial accounts can be optimized. Switching to a credit union with lower fees, opening a high-yield savings account, or consolidating accounts for easier management are all achievable during this transitional phase.

Even career decisions can be reevaluated. Remote work has made location less tied to employment, allowing many to choose places with lower taxes or a better cost of living. Some use a move as a catalyst to shift industries, start a small business, or pursue further education. The disruption of moving creates mental space to ask bigger questions: Does this job support my goals? Is my income aligned with my needs? Can I earn differently? By treating the move as a financial pivot point, rather than just a physical relocation, you gain leverage. You’re not just changing addresses—you’re reshaping your financial future with purpose.

Budgeting for the Move Without Breaking the Bank

A well-structured budget is the most effective tool for keeping moving costs under control. Without one, even modest relocations can spiral into financial strain. The goal isn’t to eliminate expenses—some are unavoidable—but to manage them deliberately. A successful moving budget includes three layers: fixed costs (like truck rental or mover fees), variable costs (packing supplies, meals on the road), and a buffer for unexpected expenses (last-minute storage, repair fees). Research shows that households who create a detailed moving budget spend, on average, 25% less than those who do not. The difference lies not in cutting corners, but in visibility and discipline.

To build an effective budget, start by listing every possible expense, no matter how small. Include both pre-move and post-move items. Pre-move costs might involve deep cleaning services, appliance repairs, or selling unused furniture. Post-move expenses include new home essentials, license or registration updates, and local transportation setup. Once listed, categorize each item and assign a realistic estimate. Use online calculators or past moving records as guides. For example, if you’re renting a truck, check multiple providers and compare rates based on distance and time. Booking early often saves 15% to 20% compared to last-minute rentals. Similarly, scheduling movers during off-peak times—mid-month or winter months—can reduce costs by up to 30%.

Tracking is just as important as planning. Use a simple spreadsheet or a budgeting app to record every expense as it occurs. This real-time monitoring prevents overspending and helps identify areas where you can adjust. For instance, if packing supplies are exceeding the budget, you might switch to free boxes from local stores or reuse old containers. Emotional spending is a common trap during moves—buying new décor impulsively or overspending on convenience services like professional organizers. A clear budget acts as a guardrail, reminding you of priorities. It also helps in making trade-off decisions, such as choosing between hiring full-service movers or doing it yourself with help from friends. While DIY moves can save money upfront, they carry hidden costs: time, physical strain, and risk of damage. Weighing these factors within the budget ensures a balanced, informed choice.

Another key strategy is saving in advance. Experts recommend setting aside funds over several months rather than paying everything at once. This reduces financial stress and avoids reliance on credit cards. Even setting aside $100 per month for six months creates a $600 cushion—enough to cover many common surprise costs. The discipline of saving ahead also reinforces financial awareness, making you more mindful of every dollar spent during the move. A budget isn’t just a list of numbers—it’s a plan for financial resilience during a high-pressure time.

Turning Expenses into Investments: The Smart Upgrades That Pay Off

Not all moving costs are losses. Some are strategic investments that generate long-term savings. The key is distinguishing between spending that depletes resources and spending that builds value. For example, paying slightly more for a home with energy-efficient windows or insulation may increase upfront rent, but it reduces monthly utility bills over time. Similarly, choosing a location with shorter commute distances can save hundreds per year in fuel, vehicle maintenance, and time—time that can be used for family, rest, or income-generating activities. These are not expenses in the traditional sense; they are financial upgrades with measurable returns.

One of the most impactful investments is in home efficiency. Installing a programmable thermostat, upgrading to LED lighting, or sealing drafts may cost $200 to $500 initially, but these improvements can reduce heating and cooling costs by 10% to 30%, according to energy efficiency studies. Over five years, that’s a savings of $1,000 or more. Some landlords even offer incentives for tenants who make such upgrades, knowing it reduces long-term maintenance costs. Another example is water-saving fixtures—low-flow showerheads and faucet aerators—which lower water bills and are often eligible for local utility rebates. These small changes, made during the move-in phase, become permanent reductions in monthly outflows.

Location-based decisions also function as investments. Paying a bit more to live near public transit reduces car dependency, cutting insurance, fuel, and parking costs. In cities with high parking fees, this alone can save $100 to $200 per month. Similarly, choosing a neighborhood with access to affordable grocery stores, healthcare, and schools reduces ongoing living expenses. These are not luxuries—they are financial optimizations. Even the decision to rent a slightly larger space can pay off if it eliminates the need for external storage, which costs an average of $150 per month. Viewing these choices through a return-on-investment lens transforms the move from a cost center to a wealth-building opportunity.

The mindset shift is crucial. Instead of asking, “How little can I spend?” ask, “Where can I spend wisely to save more later?” This approach aligns with long-term financial health. It’s not about spending more—it’s about spending better. Every dollar allocated to efficiency, convenience, or reduced future costs is a dollar working for you. Over time, these smart upgrades compound, creating a lower-cost, higher-value lifestyle that supports financial freedom.

Risk Control: Protecting Your Money During Transition

Moving introduces financial vulnerabilities that many overlook. Delays, damaged belongings, unclear lease terms, and identity risks can all lead to unexpected costs. Without proper safeguards, a single incident—a lost deposit, a stolen package, a missed bill—can undo careful budgeting. Risk control is not about fear; it’s about preparation. By identifying potential threats and implementing simple protections, you can maintain financial stability even during chaotic transitions.

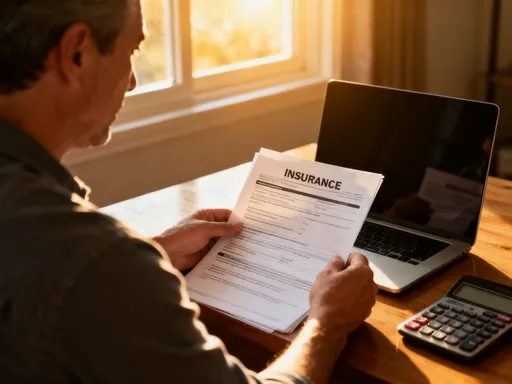

Renter’s insurance is one of the most effective tools. It covers personal property damage from fire, theft, or water leaks, and many policies include liability protection. Yet, studies show that only about 40% of renters carry it. During a move, this gap is especially dangerous. Belongings are in transit, often unattended, and more susceptible to loss. A policy that covers off-premises items ensures protection throughout the process. Review your current policy before moving—some require updates when changing addresses, and others may not cover temporary storage. Confirming coverage details prevents unpleasant surprises.

Lease agreements also require careful review. Hidden fees, unclear maintenance responsibilities, or automatic renewal clauses can lead to financial disputes. Always read the full contract, not just the rent amount. Ask about pet policies, parking rules, and late payment penalties. If possible, take photos of the unit before moving in to document its condition—this protects your security deposit. Some landlords deduct for normal wear and tear; having evidence ensures fair treatment. Additionally, verify whether the deposit is held in an interest-bearing account, as required by law in some states.

Financial logistics matter too. Update your address with banks, credit card companies, and government agencies promptly to avoid missed statements or identity theft. Use official channels—never click links in emails claiming to be from banks. Monitor accounts closely during the transition for unauthorized activity. Consider placing a fraud alert on your credit report if moving across state lines. Finally, maintain an emergency buffer—ideally one to two months of living expenses—dedicated to relocation surprises. This fund prevents reliance on high-interest credit cards if unexpected costs arise. Risk control isn’t about stopping problems—it’s about ensuring they don’t become financial disasters.

Trend Judgment: Aligning Your Move with Broader Financial Shifts

Personal financial decisions gain power when aligned with larger economic trends. Moving is no exception. The rise of remote work, shifts in housing markets, and inflation’s impact on living costs all influence the affordability and timing of relocation. By understanding these trends, you can make forward-looking decisions that enhance long-term stability. A move timed well can lock in lower housing costs, avoid rising taxes, or position you in a growing job market. Reacting to trends, rather than just personal circumstances, turns relocation into a strategic financial move.

Remote work has fundamentally changed housing choices. Without the need to live near an office, many are relocating to areas with lower costs of living, better schools, or more space. This trend has driven demand in smaller cities and suburban areas, while major urban centers see slower growth. For individuals, this means greater flexibility—and opportunity. Moving to a state with no income tax, such as Florida or Texas, can increase take-home pay significantly over time. Similarly, choosing a region with stable property values and low rent increases provides long-term predictability. These decisions aren’t just about comfort—they’re about financial advantage.

Housing market conditions also affect timing. Relocating during a buyer’s or renter’s market can lead to better deals. When supply exceeds demand, landlords are more willing to negotiate rent, offer move-in incentives, or waive fees. In contrast, moving during a seller’s market may mean higher costs and less flexibility. Monitoring local vacancy rates, rent growth trends, and economic development plans helps identify the best windows for relocation. Inflation plays a role too—rising utility and grocery prices make energy-efficient homes and proximity to affordable shopping more valuable. A move that reduces exposure to these cost drivers is a move that protects purchasing power.

Understanding these patterns allows for proactive planning. Instead of moving because a lease ends, you might choose to move when market conditions are favorable. Instead of accepting the first available option, you can wait for a better deal. Trend judgment doesn’t require predicting the future—it requires awareness of the present. By aligning personal decisions with broader shifts, you increase the likelihood of making a move that supports, rather than strains, your financial health.

Building a Post-Move Financial Routine That Lasts

The true success of a financial move isn’t measured at the end of the truck’s drive—it’s measured weeks and months later. The real win is not just surviving the transition but establishing a stable, sustainable routine in the new environment. Many people focus intensely on the move itself, only to fall back into old habits once settled. The discipline built during relocation—budgeting, tracking, decision-making—should not end with unpacking the last box. Instead, it should become the foundation of a stronger financial life.

Start by setting up banking and bill payment systems immediately. Open local accounts if needed, update automatic payments, and ensure all statements are delivered securely. This prevents late fees and maintains credit health. Next, adjust the household budget to reflect new costs: rent, utilities, transportation, groceries. Compare actual spending to estimates and make corrections. If the new area is more expensive, identify areas to reduce—dining out less, using public transit, or switching to lower-cost services. If it’s cheaper, decide how to allocate the surplus—toward debt, savings, or investments.

Building local financial habits takes time. Learn about community resources: libraries with free programs, farmers’ markets for affordable produce, credit unions with low-fee accounts. Join local groups or online forums to share tips and avoid scams. Establishing these connections fosters both financial and social stability. Most importantly, maintain the mindset of intentionality. Continue reviewing subscriptions, tracking spending, and planning for future goals. The move was a catalyst, but the progress must continue.

Over time, the discipline of the move compounds. Each smart choice—paying off debt, saving consistently, avoiding impulse spending—builds momentum. What began as a single event becomes a lasting transformation. A move, when handled strategically, is more than a change of address. It’s a financial reset, a risk management exercise, and a long-term investment—all in one. By seeing it that way, you turn a necessary expense into a powerful step toward lasting financial clarity and security.